This regulation aims to provide both fiscal and non-fiscal incentives to encourage entrepreneurs to participate in the construction and development of the IKN. Fiscal incentives are provided in the form of tax incentives, while non-fiscal incentives are provided in the form of simplified licensing procedures.

The background of this regulation is to achieve the more inclusive and equitable economic growth targets of 2045 through accelerated development in Eastern Indonesia.

1. Facilities provided in the Nusantara Capital City and Partner Regions include:

Income Tax

- Reduction of Corporate Income Tax for domestic corporate taxpayers;

- Income Tax on financial sector activities in the Financial Center;

- Reduction of Corporate Income Tax for the establishment and/or relocation of head offices and/or regional offices;

- Reduction of Gross Income for the implementation of internship, apprenticeship, and/or learning activities in the framework of human resource development based on specific competencies;

- Reduction of Gross Income for certain Research and Development activities;

- Reduction of Gross Income for donations and/or costs of construction of public facilities, social facilities, and/or other non-profit facilities;

- Income Tax Article 21 borne by the Government and is final;

- Final Income Tax of 0% (zero percent) on income from gross sales of certain businesses in micro, small, and medium enterprises; and

- Reduction of Income Tax on the transfer of rights of land and/or buildings;

Value Added Tax and/or Luxury Goods Sales Tax

The Value Added Tax and/or Luxury Goods Sales Tax facilities provided in the Nusantara Capital City include the following tax simplifications:

- Value Added Tax is not collected; and

- Exemption of Luxury Goods Sales Tax on the transfer of Taxable Goods.

Customs

The customs facilities provided in the form of customs arrangements include the following:

- Exemption of Import Duty and Facilities of Import Taxes for the import of goods by the central government or regional governments for Public Interest purposes in the Nusantara Capital City and Partner Regions;

- Exemption from Import Duty and Import Taxes Facilities for the import of capital goods for Industrial Development and Development in the Nusantara Capital City and Partner Regions;

- Exemption from Import Duty on the import of goods and materials for Industrial Development and Development in the Nusantara Capital City and/or Partner Regions.

2. Taxpayers who make investments in:

a. Nusantara Capital City

Taxpayers are granted a reduction in Corporate Income Tax in the form of:

- Corporate Income Tax reduction at 100% (one hundred percent) from the tax payable amount.

- Corporate Income Tax reduction facility can be utilized starting from the Fiscal Year when the Commercial Operations Begin.

To obtain the Corporate Income Tax reduction facility, Taxpayers must fulfill the following criteria:

- A domestic corporate taxpayer;

- Conduct business activities through a head office and/or business unit located in the Nusantara Capital City and/or Partner Regions;

- Have the status of an Indonesian legal entity;

- Undertake investment with a minimum value of Rp10,000,000,000.00 (ten billion rupiah); and

- Undertake investment:

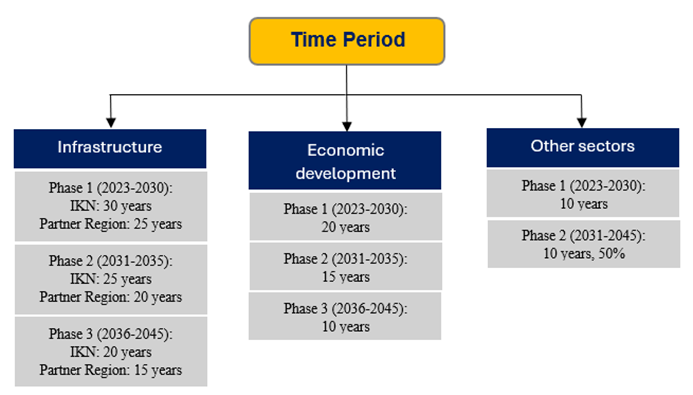

- In strategic business sectors including infrastructure and public services, economic development; and other business sectors to accelerate the development and development of the Nusantara Capital City

- In the infrastructure and public services sector in Partner Regions.

b. Partner Regions

Partner Regions are specific areas on the island of Kalimantan that have been established for the development of the Nusantara Capital City economic superhub in collaboration with the IKN Authority and are designated by Decree of the Head of the Authority. The Tax Facilities provided in the Partner Regions are:

- Corporate Income Tax reduction facility for domestic corporate taxpayers.

- Value Added Tax and/or Luxury Goods Sales Tax facilities provided in Partner Regions in the form of Value Added Tax taxation facilities are not collected.

- Customs facilities in the form of customs arrangements, including:

- Exemption from import duties and Import Taxes facilities for imports of goods by the central government or local governments for public interest purposes in the Nusantara Capital City and Partner Regions;

- Exemption from import duties and Import Taxes facilities for imports of capital goods for industrial development in the Nusantara Capital City and Partner Regions; and

- Exemption from import duties for imports of goods and materials for industrial development in the Nusantara Capital City and/or Partner Regions.

3.Domestic taxpayers who provide donations and/or costs for the construction of public facilities, social facilities, and/or other non-profit facilities in the Nusantara Capital City are granted a Gross Income reduction facility of a maximum of 200% (two hundred percent) of the amount of donations and/or costs incurred for the construction of public facilities, social facilities, and/or other non-profit facilities, which include:

- A Gross Income reduction of 100% (one hundred percent) of the amount of donations and/or costs provided; and

- An additional Gross Income reduction of a maximum of 100% (one hundred percent) of the amount of donations and/or costs provided.

4. Financial Center

Financial Center is an area designated as a concentration of financial services and a center for the development of technology and supporting services in the financial services sector.

Facilities provided at the Financial Center include Income Tax facilities for financial sector activities in the Financial Center:

- Corporate Income Tax reduction for corporate taxpayers that carry out financial sector business activities in the Financial Center in the Nusantara Capital City; and

- Facility for exemption from withholding and/or collection Income Tax on income from investments in the Financial Center in the Nusantara Capital City received or obtained by foreign tax subjects.

The corporate income tax reduction facility is granted in the amount of corporate income tax payable on a certain portion of income with percentage:

- 100% (one hundred percent);

- 85% (eighty-five percent).

The corporate income tax reduction facility is granted for:

- 25 (twenty-five) Fiscal Years, for Investments made from the year 2023 to the year 2035; and

- 20 (twenty) Fiscal Years, for Investments made from the year 2036 to the year 2045.

5. Establishment and/or Relocation of Head Office and/or Regional Office

Facilities provided for those who establish and/or move their head office and/or regional office to the Nusantara Capital City are given a corporate income tax reduction facility.

Corporate income tax reduction facilities are given at 100% (one hundred percent) of the amount of corporate income tax payable for 10 (ten) Fiscal Years. After the period of granting corporate income tax reduction ends, the corporate income tax reduction facility is given at 50% (fifty percent) of the amount of corporate income tax owed for the next 10 (ten) Fiscal Years.

6. Super Deduction Vocational and Research & Development (R&D)

a. Vocation

Taxpayers who organize and/or involve human resources in educational and/or training activities in the Nusantara Capital City for work practice activities, internships, and/or learning in the context of fostering and developing human resources based on certain competencies are given facilities including the Gross Income reduction facility is given at a maximum of 250% (two hundred and fifty percent) of the total costs incurred for work practice, internship, and/or learning activities.

The Gross Income reduction of a maximum of 250% (two hundred and fifty percent) includes:

- Gross Income reduction of 100% (one hundred percent) of the total costs incurred for work practice, internship, and/or learning activities; and

- Additional Gross Income reduction of a maximum of 150% (one hundred and fifty percent) of the total costs incurred for work practice, internship, and/or learning activities.

b. Research & Development (R&D)

Domestic corporate taxpayers who have a domicile and/or place of business activities that carry out certain Research and Development activities in the Nusantara Capital City, are provided with facilities including gross Income reduction facilities are provided for a maximum of 350% (three hundred and fifty percent) of the total costs incurred for certain Research and Development activities charged within a certain period.

Gross Income reductions of a maximum of 350% (three hundred and fifty percent) include:

- Gross Income reduction of 100% (one hundred percent) of the total costs incurred for Research and Development activities; and

- Additional Gross Income reduction of a maximum of 250% (two hundred and fifty percent) of the accumulated costs incurred for certain Research and Development activities within a certain period.

7. Article 21 Income Tax Borne by the Government and is Final

Article 21 Income Tax on income received by certain Employees is given facilities in the form of Income Tax borne by the Government and is final.

Certain Employees including Permanent Employees and Non-Permanent Employees are Employees who:

- Receive or obtain income from certain Employers;

- Reside in the Nusantara Capital City; and

- Have a Taxpayer Identification Number registered at the tax service office whose work area covers the Nusantara Capital City.

8. Final Income Tax of 0% (Zero Percent) on Income from Gross Sales of Certain Businesses in Micro, Small, and Medium Enterprises

Domestic Taxpayers excluding permanent establishments that make Investments in the Nusantara Capital City with a value of less than IDR 10,000,000,000.00 (ten billion rupiah) and fulfill certain requirements may be subject to final Income Tax at a rate of 0% (zero percent) for a certain period of time.

Final Income Tax applies from the date of approval for granting the facility until 2035.

This regulation was promulgated on May 16, 2024.

For further tax assistant please contact:

Rani Widianti

T. (+6221) 2222-0200

E. rani.widianti@shinewing.id

Alvina Octavia

T. (+6221) 2222-0200

E. alvina.oktavia@shinewing.id